In May 2026, Sam Altman made an unconventional investment offer to 169 startups.

At a Y Combinator event, he offered every startup in the latest batch $2 million worth of OpenAI tokens in exchange for equity. Not cash, tokens. Compute credits, structured as an uncapped SAFE that converts at the next priced round, the same legal instrument venture capitalists use to invest money.

Read that again. The currency of the deal was compute. A startup gives up a slice of its equity and, in return, gets inference capacity. The thing being exchanged for ownership of a company was not dollars, not a convertible note, not a service contract. It was tokens.

This should stop you, because it means compute has quietly crossed a line that most people haven’t noticed. When something can be swapped for equity in the same paperwork as cash, it has stopped being infrastructure and become a financial asset. And the Altman deal isn’t an isolated curiosity. It’s one of five things that happened in a single quarter, each marking a different stage of the same transformation.

Compute is being financialized. Right now, in real time, faster than any commodity before it.

The arc every commodity follows

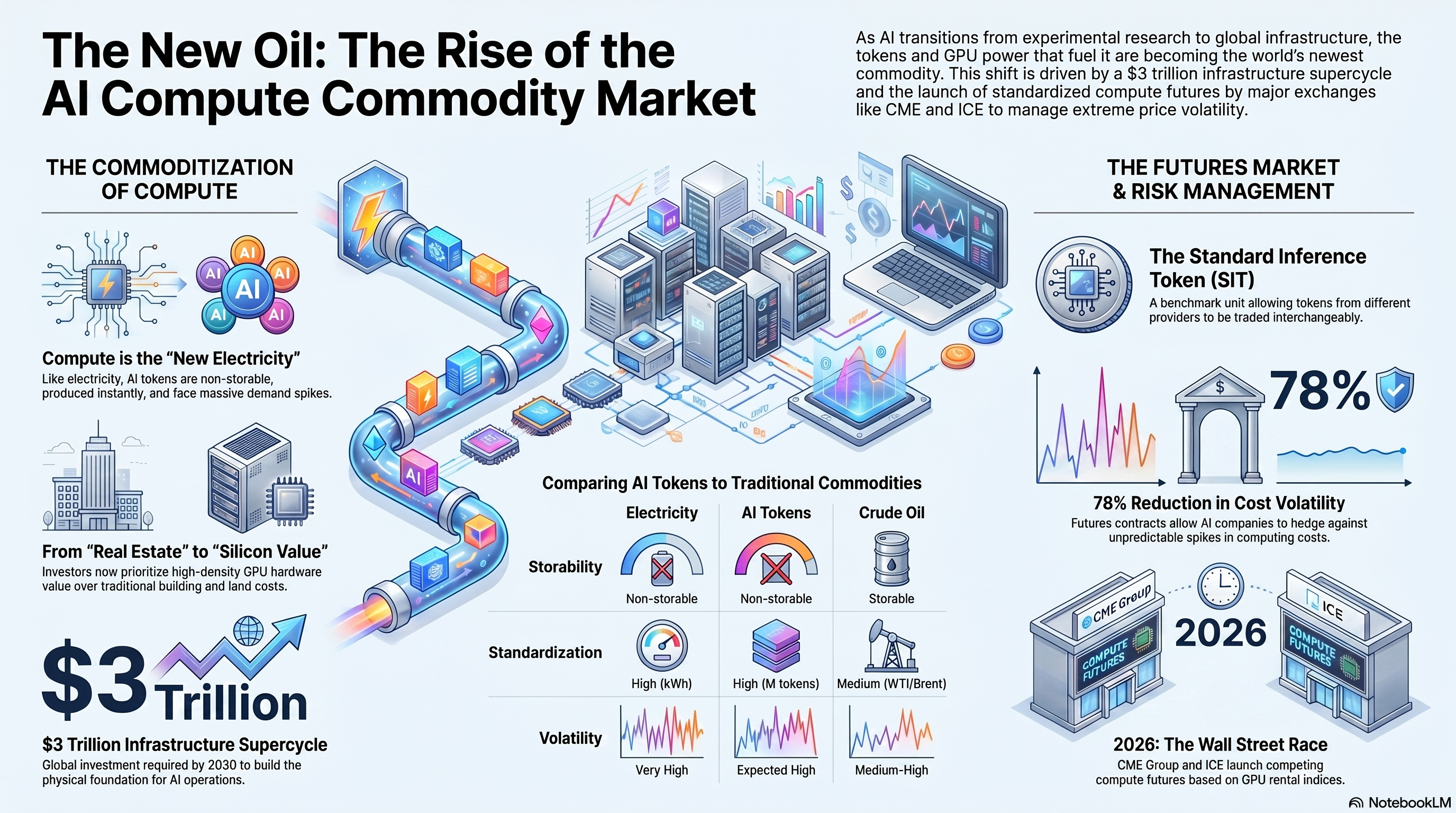

There’s a well-worn path from “useful resource” to “financial asset class”, and almost everything valuable eventually walks it.

First, the resource gets priced. A standardized unit with transparent, published rates. Then it gets traded, buyers and sellers exchange it on open markets, with derivatives layered on top for hedging. Then it gets contracted, long-term offtake agreements lock in supply at negotiated rates. Then it gets collateralized, the asset backs debt, and structured finance. And finally, it gets used as capital, a substitute for cash in financial transactions.

Oil walked this path over most of a century. Electricity took decades. Bandwidth did it in roughly fifteen years as the internet scaled. Compute is doing all five stages at once, in 2026, and the only reason it isn’t front-page news is that most people still think about compute as a line item on an AWS invoice.

Not anymore. Here’s each stage, happening now.

Priced

You can’t trade what you can’t price. For most of cloud computing’s history, the cost of compute was a bespoke negotiation. You called AWS or Google, you signed an enterprise agreement, and the rate you paid was opaque and specific to you. There was no equivalent of a posted oil price.

That changed. Silicon Data now publishes daily GPU rental-rate indices, the first standardized benchmarks for on-demand compute. Ornn publishes the Ornn Compute Price Index, distributed on the Bloomberg Terminal alongside every other asset a trader watches. These are the compute equivalents of the WTI crude benchmark or the Henry Hub natural gas price: numbers everyone can see, agree on, and build contracts around.

And the number moves. Nvidia’s Blackwell GPUs went from $2.75 to $4.08 per GPU-hour between mid-February and mid-April 2026, a 48% surge in two months. That’s not the price behavior of a stable utility. That’s commodity-grade volatility, the kind that creates real financial risk for anyone whose business depends on the resource. And where there’s price risk, financial instruments follow.

Traded

In May 2026, both of the world's largest derivatives exchanges announced compute futures.

CME Group, the world’s leading derivatives marketplace, partnered with Silicon Data to launch a compute futures market built on those daily GPU rental indices. CME’s chairman put it plainly: compute is “the new oil of the 21st century”. A week later, the Intercontinental Exchange, parent of the NYSE, announced its own GPU compute futures based on Ornn’s price index.

These weren’t the first attempts. Architect Financial Technologies had already launched perpetual futures on GPU and RAM prices, and the prediction market Kalshi was letting users wager on Nvidia compute prices. But CME and ICE are a different category of event. They bring institutional liquidity, regulatory credibility, and the clearing infrastructure that turns a niche product into an asset class. When CME listed crude oil futures in the 1980s, it didn’t invent oil trading; it legitimized it, standardized it, and made it something every institution could participate in. That’s what’s happening to compute now.

There’s even academic scaffolding for it. A March 2026 paper argued that inference tokens are transitioning from “intelligent service outputs” to “compute infrastructure raw materials”, and analyzed how to design derivatives contracts around them, drawing direct parallels to electricity, carbon allowances, and bandwidth. The theory is catching up to the trading desks.

Contracted

Spot prices and futures are half of a commodity market. The other half is long-term supply contracts. The offtake agreements that let a buyer lock in years of supply and a seller finance the build-out. And compute is now being contracted exactly like energy.

Google is paying SpaceX $920 million per month, from October 2026 through June 2029, for access to roughly 110,000 Nvidia GPUs. Anthropic signed a similar deal: $1.25 billion per month through 2029 for the full capacity of SpaceX’s Colossus 1 data center. These contracts have everything an energy offtake agreement has: multi-year terms; ramp-up schedules; cancellation clauses with 90-day notice; delivery penalties; and grace periods. This is not the language of a cloud invoice. It’s the language of a power purchase agreement.

Two details make the point unmissable. First: the seller is a rocket company. SpaceX, weeks before the largest IPO in history, is one of the world’s largest lessors of GPU capacity. When a space company becomes a compute landlord, you are watching an asset class form. Second: the buyer is Google, by some measures the largest single owner of AI compute on earth, and it still had to lease, because demand for its Gemini Enterprise agent platform outran even its own enormous supply. When the biggest owner doesn’t have enough, scarcity is structural, and structural scarcity is what drives everything downstream.

The capital numbers match the framing. Alphabet has committed more than $180 billion in capital expenditure for 2026, expects that to rise significantly in 2027, and raised $80 billion in equity to help fund it. Those are energy-sector numbers, the kind of capital intensity you associate with building pipelines and power grids, not with software.

Collateralized

Once an asset has predictable contracted cash flows, you can borrow against it. And compute is now backing debt at scale.

CoreWeave pioneered the structure: isolate the GPUs, the customer contracts, and the facilities into discrete cash-flow units, then finance each unit against its contracted revenue. By treating compute as a financeable asset rather than a depreciating expense, CoreWeave raised roughly $28 billion in combined debt and equity over a year. In Australia, Firmus Technologies signed a $10 billion GPU financing facility backed by Blackstone, structured against long-term customer contracts, project finance for silicon, identical in shape to how you’d finance a toll road or a power plant.

One managing director at a global infrastructure fund described the mental shift better than I could: “We are no longer underwriting property. We are underwriting silicon. The walls and the roof are just the packaging for the most expensive, fastest-depreciating asset class on earth.”

GPU-backed lending, GPU lease financing, asset-backed securities for compute, the entire toolkit of structured finance is being rebuilt around chips. The financial plumbing is being laid while everyone watches the models.

Used as capital

Which brings us back to Altman.

His tokens-for-equity offer is the final stage of the arc, the one that completes the transformation. Once an asset is priced, traded, contracted, and collateralized, the last thing it becomes is money, a substitute for cash in financial transactions. Altman didn’t sell compute to those startups. He invested it, in exchange for ownership, in the same instrument a VC would use to deploy a fund.

And there’s a layer underneath that most of the coverage missed. Inference costs are falling roughly fourfold per year. The tokens Altman is handing out today will cost OpenAI dramatically less to produce by the time those SAFEs convert into equity at a Series A. He is issuing a rapidly depreciating liability in exchange for a potentially appreciating asset. That’s not generosity, and it’s not just lock-in. It’s an arbitrage, the kind of trade you can only run once your product has become a financial instrument with predictable cost curves.

When compute becomes capital, the company that produces it most cheaply becomes something like a central bank for the agent economy. That should make you think hard about who you take tokens from.

Why this matters for everyone building

Step back from the individual deals, and the picture is bigger than finance.

For builders, financialization is good news that sounds like bad news. The single most unpredictable cost in running an AI company is inference, and unpredictable costs make it impossible for businesses to plan. Futures markets fix this. When you can hedge compute the way an airline hedges jet fuel, you can lock in your largest variable cost and actually model your unit economics. Every previous internet business scaled on the back of predictable infrastructure costs, predictable bandwidth, and predictable hosting. The agent economy needs predictable compute, and futures markets are how it gets there.

For the agent economy specifically, this is the missing supply layer. I’ve argued in earlier essays that agents will route around consumer apps to talk directly to infrastructure, that transaction costs are collapsing toward zero, and that the agent economy now has a payment rail. A functioning agent economy needs three things: a way to pay (payment rails), a way to coordinate (APIs), and a reliable, priceable supply of the one resource agents consume (compute). Two of those three already exist. The financialization of compute is the third clicking into place.

And for the broader economy, compute is becoming what oil was to the twentieth century, the strategic resource around which geopolitics, corporate strategy, and financial engineering all rotate. Export controls on GPUs are already a foreign-policy instrument. Sovereign compute reserves are already being discussed in capitals. This stopped being a technology story a while ago. It’s a macroeconomic one now.

What could break it

I don’t want to narrate this as a smooth inevitability, because the risks are real and large.

Obsolescence is the structural problem: GPUs depreciate on a roughly 36-month cycle. Financing a fast-depreciating asset at energy-infrastructure scale is genuinely novel, and the lenders doing it are underwriting collateral that can lose much of its value before the loan matures. If hardware cycles accelerate, a lot of asset-backed compute debt could go underwater fast.

Concentration breaks the commodity story: A real commodity market has many producers. Compute has essentially one. Nvidia controls the underlying hardware that every one of these futures, contracts, and loans ultimately depends on. A commodity market with a single supplier isn’t quite a commodity market; it’s a pricing dependency wearing a commodity’s clothes. What happens to compute futures if Nvidia changes its allocation strategy?

Demand might not be real: The entire edifice assumes that $750 billion a year in AI capex reflects durable demand. If it’s a supply-side overbuild, capacity racing ahead of actual usage, the parallel isn’t oil. It’s the late-1990s fiber-optic boom, where enormous infrastructure was financed against demand that arrived years later than the debt was due, and a lot of capital was destroyed in between.

The regulators haven’t shown up yet: Compute futures, GPU-backed securities, tokens-as-equity, none of this sits cleanly inside an existing regulatory framework. Is a compute future a commodity derivative the CFTC oversees? Are tokens-for-equity deals a securities matter for the SEC? Nobody has decided, and the gap between financial innovation and regulatory clarity is exactly where past crises have grown.

The speed is the story

Compute is following the same path oil, electricity, and bandwidth all followed: useful resource to scarce resource to priced, traded, contracted, collateralized, and finally monetized as capital. None of the individual steps is unprecedented. What’s unprecedented is the compression. Oil took a century to walk this path. Compute is doing it in a single quarter.

By the time most people register that compute has become a financial asset class, the futures will already be trading, the offtake agreements will already be signed, and the tokens will already be converting into equity on cap tables. The infrastructure of the agent economy isn’t just being built. It’s being financialized in the same breath.

Which means the people building the financial layer, the indices, the futures, the lending structures, the token-as-capital deals, are going to matter as much as the people building the models. Maybe more. The model is the product. Compute is the asset. And assets are where the real money has always been made.

If you’re building in compute markets, pricing, derivatives, financing structures, or token-based instruments, I want to hear about it. Reply to this email or find me on LinkedIn.